It's clear that, with our relative strength in financial services, Australia has the potential to become a leading FinTech player. That means getting the policy settings right and backing local FinTech firms to maintain and develop competitive advantage and global leadership.

The Government's FinTech program both promotes Australia as a hot house for financial services and showcases our innovative financial products and services to the world.

Our policies and regulations will also help promote Australia's FinTech capability by supporting the evolution of our FinTech start‑ups and innovators to develop, test and globally launch their innovative financial products and services. Australia's dynamic ecosystem will help our burgeoning start‑up community to foster innovation and turn these ideas into commercial opportunities and successful commercialisation. Australia can then serve as a launching pad into Asia and other overseas markets.

The Government is committed to working with the FinTech industry, regulators and other stakeholders, on the key issues to underpin the continued innovation in financial services. We will support the industry's objective of making Australia the leading market for FinTech innovation and investment in Asia by 2017.

We are setting out a clear strategy and agenda for the FinTech sector, based on the issues identified by the sector. The Government will consider these issues in collaboration with the industry and other key stakeholders, including regulators.

While Australia's regime is well‑placed, we know there are still many opportunities to grow stronger.

Together, we are looking ahead to an exciting and growth‑driven future in the sector. The Government will build on actions we have taken through our response to the Financial System Inquiry by focusing on areas relevant to FinTech including the following areas.

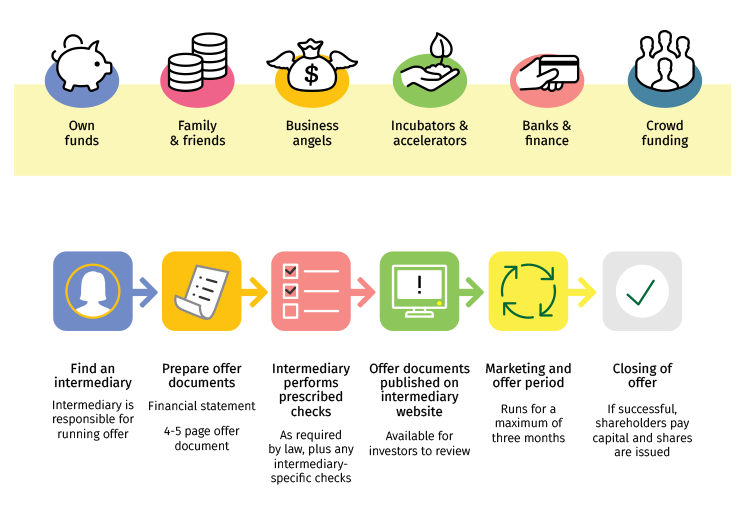

Crowdfunding

The Government recognises the growth and expansion of crowdfunding, and a framework for Crowd‑Sourced Equity Funding (CSEF) was introduced into Parliament on 3 December 2015. Our CSEF framework will allow eligible Australian public companies to access new funding sources to help them develop their ideas.

Following implementation of the Government's CSEF framework, the industry is keen to explore how the framework can evolve over time.

In addition to the CSEF framework, the industry has asked the Government to explore the potential for crowdfunding to extend to debt funding. The Government intends to consult on a crowd sourced debt funding framework during 2016.

Industry has also raised possible extensions to the framework that could improve access to finance for new FinTech firms so that they can develop and commercialise new ideas. It has been put to the Government that the CSEF framework:

- Allow all companies regardless of assets and turnover to be eligible for equity crowdfunding.

- Remove cooling off periods and allow platforms to use their discretion to cancel an investment for legitimate reasons.

- Review Australian Market Licence (AML) requirements for crowdfunding intermediaries.

The Government will continue to work with industry to ensure that Australia has a competitive and commercially attractive crowdfunding framework that deepens capital markets across the economy. Following further consultation with the industry, including the FinTech Advisory Group, the Government will consider:

- increasing the assets and turnover threshold used to determine eligibility for equity crowdfunding to $25 million; and

- reducing the cooling off period for investors into crowd‑sourced equity funded projects to 48 hours.

Comprehensive credit reporting

Access to comprehensive credit reporting (CCR) data would help facilitate the development of peer‑to‑peer lending products and marketplaces, and help drive further innovation in financial services. CCR is considered by many to be a vital part of Australia's economic infrastructure.

CCR provides lenders with more information to identify a customer's true credit capacity to enable more tailored lending that better reflects the capacity to service and repay loans.

To encourage the utilisation of CCR, the Government has tasked the Productivity Commission with consideration of the up‑take of CCR as part of its inquiry of data accessibility.

The Government is keen to support industry efforts to expand the access and utilisation of CCR across the economy. The Government will monitor progress and evaluate uptake of CCR and will consider other options if required.

Greater availability of data

Effective use of data is increasingly integral to the efficient functioning of the economy. Improved availability of data, combined with the tools to exploit it, is creating new economic opportunities.

In line with our Public Data Policy Statement, we will make data.gov.au the central place for all government data. Non‑sensitive data will be open by default — providing free access to public data, where fees only apply for specialised data services. This will support private sector innovation to create new products and business models, as well as inform government policy making and service delivery.

In addition, the Government has commissioned the Productivity Commission to examine the benefits and costs of improving availability and the use of data across the economy. This will inform Australians about the potential for data availability to boost innovation in Australia to help us remain globally competitive.

The industry is seeking more standardised practices on financial data aggregation and government support for standard open‑data application programming interfaces (APIs) to support FinTech innovators and give Australians better ways to understand, manage and maximise their finances. The Productivity Commission will examine options for standardising the collection, sharing and release of data as part of its inquiry.

Regulatory environment that enables innovation (regulatory sandbox)

We need a regulatory environment that provides consumers with confidence while not unnecessarily restricting the opportunities for innovation.

A 'regulatory sandbox' has the potential to encourage and support the design and delivery of new financial products and services that benefit consumers and businesses. The industry believes that a 'sandbox' is a crucial component to assist Australia become a leading market for FinTech innovation in Asia.

The Government has been working with the Australian Securities and Investments Commission (ASIC) on the development of a 'regulatory sandbox' for Australian FinTech start‑ups.

With a 'regulatory sandbox', FinTech innovators can overcome regulatory uncertainty and costs that may otherwise see innovative offerings not go ahead. According to the industry an effective 'sandbox' will enable firms to manage regulatory risks during the testing stage, reducing the cost and time to market. At the same time, any 'sandbox' will need to provide for important consumer outcomes such as fit and proper checks, dispute resolution and consumer redress arrangements.

Australia's regulatory regime is flexible in terms of delivering licensing and regulatory oversight tailored to the scope of a start‑ups business, while ensuring consumers remain informed. The legislative framework makes it possible for ASIC to grant waivers (or relief) from the law to facilitate business.

The Government believes that Australia's financial system can support a 'regulatory sandbox' for the FinTech industry. ASIC has well‑established policies in place for the use of its waiver (relief) powers. At a minimum, the existing flexibility and responsiveness of our regulatory arrangements can help reduce the regulatory barriers, and the cost of licensing for new businesses and products entering the market. For example, the existing ASIC class waiver for low‑value, non‑cash payment facilities has been important in facilitating businesses operating such types of payments.

During 2014–15, ASIC approved 1,473 relief applications. Among other matters, existing waiver powers enable ASIC to grant relief from Australian Financial Service (AFS) licensing requirements, provide exemptions from disclosure or reporting obligations, and issue no‑action letters where ASIC does not intend to take regulatory action over a particular instance of non‑compliance.

Australia's regulatory regime also compares well in terms of how long it takes to make a decision. ASIC has an average target of 60 days to grant a credit or financial services licence compared to the United Kingdom, which aims to make a decision within six months.

Start‑ups can also find it difficult to navigate the complexity of financial services laws, which is time consuming and expensive. The Government is committed to making this easier.

In April 2015, ASIC established an Innovation Hub to help FinTech start‑ups navigate the regulatory laws it administers on a streamlined basis, including by providing informal guidance from senior regulatory advisers. Since then, the Hub has accepted requests for assistance from 52 entities and has worked closely with other domestic and international regulators.

ASIC's Innovation Hub is currently working with its Digital Finance Advisory Committee on how to best utilise the existing regulatory arrangements and what further measures should be considered. The Government will support ASIC and other regulators on the development of a 'regulatory sandbox' and other facilitative measures that will help position Australia as a leading market for FinTech innovation and investment in Asia.

Technology neutrality in financial regulation

As part of the Government's response to the Financial System Inquiry, we committed to amending priority areas of existing financial regulation to ensure they are technology neutral. We will also embed the principle of technology neutrality into our approach for making future legislation and regulations.

Adopting a technology neutral approach to regulations will enable businesses to adopt approaches that best suit their business model and consumer preferences. It will also ensure that regulators can readily respond and adapt their oversight to take account of innovation and development of new technologies.

Guidance on robo‑advice

The Government is supporting regulatory authorities and the industry on the development of clear guidance on the compliance obligations for digital or automated financial advice known as robo‑advice.

Existing regulatory guidance contemplates robo‑advice; however it does not address some of the specific issues which are unique to robo‑advice. New guidance will provide clarity on these issues and how to satisfy the 'best interests' requirement of financial advice in a robo-advice context.

Greater clarity around how the existing regulatory framework interacts with the emerging robo‑advice sector will help reduce costs for the FinTech industry, improve compliance and reduce unintentional breaches of the regulations.

The Government is working with ASIC to determine necessary updates to current guidelines in order to facilitate the uptake of robo‑advice. In particular, the Government supports ASIC's draft regulatory guidance released today, 21 March 2016, that clarifies how 'best interests' duty obligations could work for robo‑advice and that ASIC will continue to provide up to date advice and guidance to the FinTech industry.

Digital currency — GST treatment

The Government recognises that that the current treatment of digital currency under GST law means that consumers are 'double taxed' when using digital currency to buy anything already subject to GST. The Government is committed to addressing the 'double taxation' of digital currencies and will work with the industry on legislative options to reform the law relating to GST as it is applied to digital currencies.

Currently, there are more than 600 digital currencies available, with different protocols for transaction processing and confirmation, and with different approaches to the growth in the supply of digital currency units. Removing the 'double taxation' treatment for GST on digital currencies and applying adequate anti‑money laundering and counter‑terrorism financing rules may facilitate further developments or use in the future.

Blockchain technology

Blockchain is a name for the protocol underpinning Bitcoin, as well as other digital currencies. It uses complex cryptography and a distributed ledger —or copies of the same record in multiple places — to regulate, record and enable transactions using Bitcoin.

Blockchain has attracted considerable interest in, and is currently being applied to, a number of areas within the international financial system and may revolutionise key services like international transfers between banks, equities clearing and settlement, and financial contracts.

The Government welcomes the announcement by the ASX that it is exploring Blockchain technology for a new post‑trade solution for the Australian equity market. While it is in the early stages of development, the technology has the potential to radically simplify the way our market operates end‑to‑end, with significant benefits to investors, participants, regulators and government agencies.

Government procurement and service delivery (ProcTech)

As financial services become more globalised and technological disruption becomes more prevalent, Australia needs to keep pace with innovation in banking and finance to stay competitive, and regulators and governments have to play their part.

This not only means ensuring our regulatory processes do not suffocate these developments, but that we also look for ways to tap into the significant opportunities afforded by FinTech to provide solutions to Government procurement and service delivery needs.

Just as alignment and modernisation in regulation is referred to as 'RegTech', the potential impact of FinTech on government procurement can be referred to as 'ProcTech'.

According to the latest Department of Finance report, there were over 69,000 Commonwealth Government procurement contracts valued at $60 billion in the 2014–15 financial year.

The Commonwealth will be looking to innovative FinTech solutions to foster diversity, choice and responsiveness in government services. 'ProcTech' can help encourage innovation, entrepreneurship and more efficient investment, providing greater value for tax payer money and potential savings that can be re‑directed into vital services.

FinTech also provides the opportunity for payment systems processes to become more modern, efficient and simple to use. As proven by developments overseas, FinTech can provide customers with more convenient mobile payment systems, with smaller processing costs that are safer and more transparent. The Government welcomes these developments in the financial system, and recognises the potential benefits these services offer to government agencies and departments.

The Government supports reviewing the uptake of FinTech services by public agencies and recognises the potential FinTech provides to improve customer experiences and make processes cheaper, more timely and secure.

FinTech is important to ensuring Australia's financial framework is world class and able to provide Australian businesses and customers with an improved user experience. This applies equally for customers and suppliers to government, as it does to parties transacting in a commercial environment. Faster and more transparent payment systems offer tangible benefits to those transacting with government, and ensures the users can be confident that public authorities are using the most secure and efficient systems available.

The Government recognises that for some services Australia still relies on manual processes, which can lead to inefficiencies, inconsistencies, and occasional errors or transactional back‑logs. We are aware that other countries have achieved significant cost savings by adopting new technologies, such as electronic payment systems, and we are committed to understanding how such improvements could benefit Australia.

The Government is excited by the potential for FinTech to provide enhancements to current systems, by contributing to higher user satisfaction, transparency and accountability, reduced administrative burdens and gains in efficiency.

Cyber security

Strong cyber security is essential to allow individuals and businesses to take advantage of the economic possibilities of the digital world. To create opportunities for businesses in the rapidly growing cyber security sector, we're providing $30 million through to 2019–20 to establish a new industry‑led Cyber Security Growth Centre to grow and strengthen Australia's cyber security industry.

The Cyber Security Growth Centre will facilitate improved engagement between research and business, improved access to global supply chains and international markets, improved management and workforce skills, and regulatory reform.

The global cyber security market is currently worth more than US$71 billion and is growing at around eight per cent a year. A Cyber Security Growth Centre will ensure that Australia is a global industry leader, able to export products and services in the global marketplace while helping Australian businesses and governments to address the growing threat of cyber‑crime.

Domestic non‑AUD settlements

New payment FinTech firms require cost effective access to non‑AUD settlement infrastructure. This ensures that they operate with the acquiescence of a foreign bank/custodian authorised deposit taking institution that may not be disposed to servicing either a disruptor, or non‑resident entity with a particularly complex risk profile. Improving access will lead to improved opportunities for Australian FinTech, and better consumer outcomes.

Insurance

It is easy to get excited about FinTech's possibilities to create a more efficient financial system. Better information through big data can transform daily interactions by consumers with financial products and services, especially insurance. Take car insurance for example, where most policies are purchased on an annual basis based on an estimate of our risk profile as a driver. FinTech allows the maker of a navigation device to partner with insurance companies. This would allow bespoke and personalised policies on demand based on a proposed route. The insurance premium would then take into account if the proposed route took a high accident route or a quiet street. Rather than insuring an asset over a fixed period of time, technology presents a different way of underwriting risk.

The FinTech industry would like the Government to support increased flexibility to support emerging micro‑insurance and quasi insurance models (e.g. self‑funded excess and peer‑to‑peer insurance) which are not readily facilitated by current models.