Downloads

***Check against delivery***

Introduction

The IMF and World Bank Spring and Annual meetings are always an important time for international economic policymaking and co-operation, and this week is no exception.

As many of you will have seen, G20 Finance Ministers and Central Bank Governors have just released their communique.

This was a successful G20 meeting, notwithstanding intense debate, reflected in this morning's combined G20/IMFC meeting, on IMF reform. But more about that in a moment.

As you know, in Sydney in February, G20 Finance Ministers and Central Bank Governors made a commitment to boost global growth by at least 2 per cent above the current trajectory over the next 5 years. The G20 members have today committed that these will be new actions, that will:

- go beyond previous G20 commitments;

- address identified gaps in individual country's policy settings;

- rebalance, as well as lift, global demand, while also boosting potential growth and enhance exchange rate flexibility; and

- create substantial positive spillovers, so that the net effect will be greater than the sum of individual country impacts.

Structural reforms which open up product and service sectors to greater competition and boost productivity, along with trade enhancing measures and competition policy initiatives, will be critical. Such measures will be complemented by action to promote and prioritise quality investment, especially in infrastructure.

Of course, these commitments have yet to be turned into actions, with the country growth strategies to be delivered by Leaders at the Brisbane Summit in November.

But by being more explicit in their commitments and through their intention to review the growth strategies in the September meeting, G20 members have raised further the cost of failure, and given themselves even more of an incentive to put forward real, concrete initiatives.

Today, however, I want to take a step back to look at the cornerstones of the international architecture and the reason we are here—the IMF and World Bank Group—to consider how well they serve us.

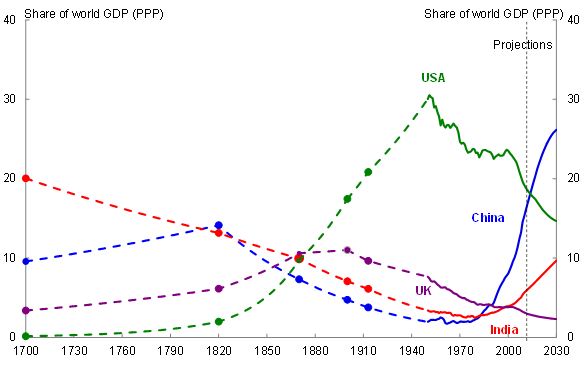

The global economic backdrop has undoubtedly changed significantly since these institutions were established. The centre of global gravity, which had been shifting from Asia to the West since the Industrial Revolution, is now returning to the Asia-Pacific region. Along with this shift we are also seeing a dispersion. The world is no longer unipolar with a clear single centre; the centres of growth are increasingly spread across a range of hubs.

Chart 1 – Share of world GDP for US, UK, China and India

As a result, we're seeing emerging market countries that are increasingly standing on their own two feet. They're contributing a growing share to global output and, with it, are exercising—or at least, are expecting to exercise—a growing degree of influence. This is inevitably having implications for the global economic architecture and its institutions.

The emergence of the G20 is a good example of this. As a forum, it emerged as a consequence of the Asian Financial Crisis, and morphed into a Leader-led process as a result of the Global Financial Crisis. It has the right membership for the new global reality, including advanced and emerging market economies.

The Bretton Woods institutions

But what of the Bretton Woods institutions? In short, I believe they have generally served the global economy well. When comparing the inter-war period with the post-World War II era, the lesson is that global economic growth and stability requires international coordination – coordination that has been made possible by the Bretton Woods institutions.

Some suggest that the original circumstances which prompted the creation of the Bretton Woods system are no longer relevant today, and to some extent I see their point.

The international economic system with both floating and fixed currencies, the greater use of market-based policies and additional flexibility does not call for the same type of exchange rate co-operation that was needed in 1944. Today, emerging market economies and others are able to use domestic policies and their own financial resources as buffers against the risk of currency crises.

Similarly, countries have much easier access to private sources of finance. In coming years, the bulk of the world's poor will live in middle-income countries that are not eligible for the main form of World Bank financing.

However, while the specific circumstances have changed, the rationale for these institutions is still just as strong. In fact, in a world where globalisation has created more international connections than was even imaginable 70 years ago, the need for effective global institutions of this sort is greater than ever – but I emphasize the word effective.

The ongoing need for the IMF and the World Bank

The principle underlying the Bretton Woods organisations is that global economic growth and stability is a global public good that both benefits, and requires the participation of, all members of the global community.

Today, the intricate networks of trade, finance, people, and confidence channels have created a world where a country's economic circumstances don't simply affect itself. This applies equally to both the negative spill-overs from financial and economic crises, and the positive spill-overs from policy coordination and more widely dispersed economic growth and development.

Looking first at the IMF, the lending it provides in crisis situations has restored confidence, credibility, and prevented crises from having much more severe contagion than ultimately eventuated. That said, the role it plays as the cornerstone of the global financial safety net cannot be taken for granted – a point I will come back to shortly.

Meanwhile, the World Bank is the world's foremost organisation for providing direct development assistance, as well as being a focal point for global development efforts.

Both institutions also fulfil a vital need, by simply providing forums and vehicles to share economic experience and expertise. It's easy to criticise these little more than a “talk shop”, but the importance of economic dialogue – the sharing of lessons and experiences - cannot be overstated.

The important feature is that the benefits from these activities accrue to more than just individual countries themselves. The trade, labour, and technology flows associated with faster economic development extend beyond the borders of aid-recipient countries. Likewise, the benefits of a stable and functioning international financial and economic system lift global growth by more than the growth impacts experienced by any single country.

While the benefits from international cooperation in these areas do not, de facto, mean the IMF and World Bank are best placed to provide it, their well-established place in the global architecture and their broad-based membership are comparative advantages that should not be lightly discarded.

With 188 members, the IMF brings together the broadest possible spectrum of countries, perspectives and approaches – a diverse membership that has taken the past seven decades to establish. This diversity means it is uniquely placed to assess global risks and policies in a way which simply cannot be replicated at a regional level.

Similarly, the World Bank brings together the world's major lenders and borrowers, enabling a consistent global strategy for development.

Current and future challenges

In saying this, these institutions are not perfect. Their scorecards are not unblemished and they face challenges – a point I've been making to this gathering, and more broadly, f

or well over a decade.

One example for the IMF is its programs in the midst of the Asian Financial Crisis, which have been picked over in great detail in the intervening years. Some argue these programs were effective in managing the crisis, others the opposite. But, regardless, that period undoubtedly damaged trust in the IMF within emerging Asia – a distrust that has seen Asia shy away from both accessing and supporting the established IMF safety net, at a cost both to the countries themselves and to the IMF.

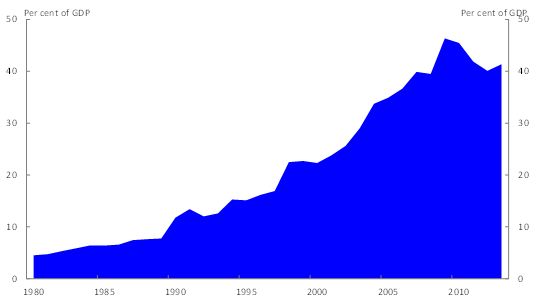

This is illustrated by the preference throughout Asia for self-insurance via foreign exchange reserves. The build-up of reserves is imposing high intermediation and transaction costs on their economies, representing a deadweight loss to these countries. It's also distorting global resource allocation. The build-up is causing large amounts of public savings to be directed towards investment in US dollar assets in the advanced world, which are “recycled” to emerging markets by advanced economy investors seeking returns on riskier investments.

Chart 2 – Foreign exchange reserves of emerging Asia

Note: Emerging Asia is China, Hong Kong, Indonesia, Korea, Malaysia, Singapore and Thailand.

Source: IMF

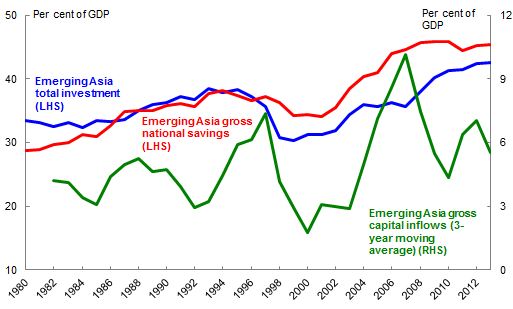

Chart 3 – Gross savings, investment and capital inflows

Note: Emerging Asia is China, Hong Kong, Indonesia, Korea, Malaysia, Singapore and Thailand.

Source: IMF

The World Bank, too, is open to criticism: for neglecting the human impact of its programs; and its strong focus on state actors rather than the private sector; while the perception of heavy influence by a small number of powerful nations is, as with the IMF, undermining its credibility with other countries. Furthermore, the bureaucracy of the World Bank, and the time taken to get projects approved, can dramatically slow the pace of development and reform.

In addition to these institution-specific challenges, the rise of the emerging market economies is creating challenges across both institutions.

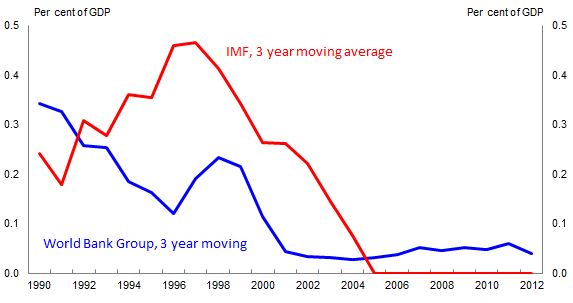

One is that the use of global public sector financing as a tool to influence domestic policy and development strategies is becoming less important as emerging economies have increasingly robust growth and established financial buffers. We can see this partly in the decline of lending by the World Bank and the IMF to emerging Asia since the late 1990s.

Chart 4 –World Bank Group and IMF lending to emerging Asia

Note: Emerging Asia is China, Hong Kong, Indonesia, Korea, Malaysia, Singapore and Thailand.

Source: IMF WEO, World Bank, Treasury calculations

Secondly, with the rise of the emerging markets, there's a growing network of regional, bilateral and domestic forums seeking to achieve similar goals to the Bretton Woods institutions. This in part reflects emerging markets' experiences with these institutions in the past—as in the case of the Asian financial safety net mentioned earlier—as well as a simple reflection of the growing economic power of these economies. As they grow, they're naturally tending towards forums and institutions that reflect their needs and respond to their voices.

While these regional and plurilateral institutions have the potential to complement the global institutions, it must also be acknowledged that they have the potential—and at this stage I do believe it is only potential—to undermine the Bretton Woods institutions if those institutions are unable to evolve and adapt.

What is needed going forward

Given these challenges, how can the IMF and the World Bank adapt to remain relevant and fit for purpose for emerging markets in today's world? Efforts have begun, but ensuring success will require continued and more concerted effort.

First and foremost, the Bretton Woods institutions need to adapt to ensure they better represent the global economic landscape as it currently is—not how it was half a century ago. Only when these institutions give their members voices that more closely reflect their relative geoeconomic positions can the institutions be more universally viewed as being legitimate, balanced and effective.

It is for this reason that Treasurer Hockey mentioned to this gathering only a couple of days ago, his deep disappointment that the 2010 IMF quota and governance reforms have still not been implemented and that the path forward for ratification is now highly uncertain.

The failure of Congress to deliver these reforms is doubly galling to other countries given the US' strong and aggressive championing of these reforms when they were first proposed.

G20 and IMFC member countries see the US as the critical obstacle to improving the credibility and legitimacy of the IMF. Continued failure on the part of Congress will increasingly see US leadership questioned, and erode countries' commitment to the global architecture which the US has championed over 70 years.

But it's not just quota and governance reform that is needed—the IMF and World Bank both also need to adapt and evolve their current practices, mindsets and cultures.

Here, at last, we can see some progress. But while the initial efforts to refresh the two institutions, such as through the World Bank's 'Global Practices' and the IMF's post-Global Financial Crisis credit lines, are promising, more needs to be done to create genuine partnerships, especially with emerging market economies.

Finally, it's important to remember that, in a perfect world, a successful IMF and World Bank would not lend any money. Effective policy advice and surveillance would prepare us for crises before they occur and establish paths towards sustainable, inclusive growth. The metric for success and relevance within these institutions should not be the size of the cheque.

As was again evident this morning, at the combined IMFC/G20 meeting, the G20 will continue to be a driving force for reform to the two Bretton Woods Institutions because the G20 membership understands the fundamental role they play in delivering development and financial stability.

While it may be uncomfortable to acknowledge, the burden of responsibility for ensuring these institutions remain central to the global architecture is, at least initially, on advanced economies, especially advanced economy G20 members. Australia remains committed to this, but leadership and commitment from the large global players, especially the United States, is required.

But responsibility does not stop with the advanced economies. The key beneficiaries of reform are the emerging market economies and, to be frank, key emerging market economies could play a more active and focused role in raising pressure on the United States Congress to ratify the 2010 IMF reforms.

Conclusion

Some 70 years ago at Bretton Woods the foundations of the IMF and the World Bank were laid. These foundations were built on the idea that international cooperation is a global public good, and this principle remains as true now as it was back then.

But, as the world has changed, these institutions have not kept pace. Insufficient effort has been put into refreshing and adapting their business to ensure they remain suited to today's global economy.

Undoubtedly, global institutions are by their nature slow moving beasts. But we must push them to adapt—if they fail to fit the circumstances of the emerging world, the costs will be felt by us all. This is a message that has to be repeated, and repeated a

gain, if we are to make progress.

Thank you.